Current State of Downstream Master Limited Partnerships and M&A Activity in 2016

Master Limited Partnerships (MLPs) have been around for decades. However, in 2008, the IRS ruled that certain downstream energy assets, such as wholesale fuel sales to end users (dealers) and real estate associated with downstream assets, would qualify for MLP treatment. This served as a catalyst to spur investment and organizational structures to take advantage of the tax advantage offered by MLP entities. Since then, multiple downstream MLPs have issued units to investors in the capital markets.

Like buying a stock, anyone with a brokerage account can invest in an MLP. There are some noteworthy differences between an MLP and a traditional stock though. As opposed to issuing shares like most publicly traded companies, MLPs issue units. The main difference between units of an MLP and shares of a public company is that earnings from an MLP do not incur corporate taxes, the majority of the earnings are distributed to the unit holders, and such distributions are taxed at the unit holder level. In other words, there is a ~35% savings off the top for investors receiving distributions from their MLP units vs. dividends from a public company’s shares.

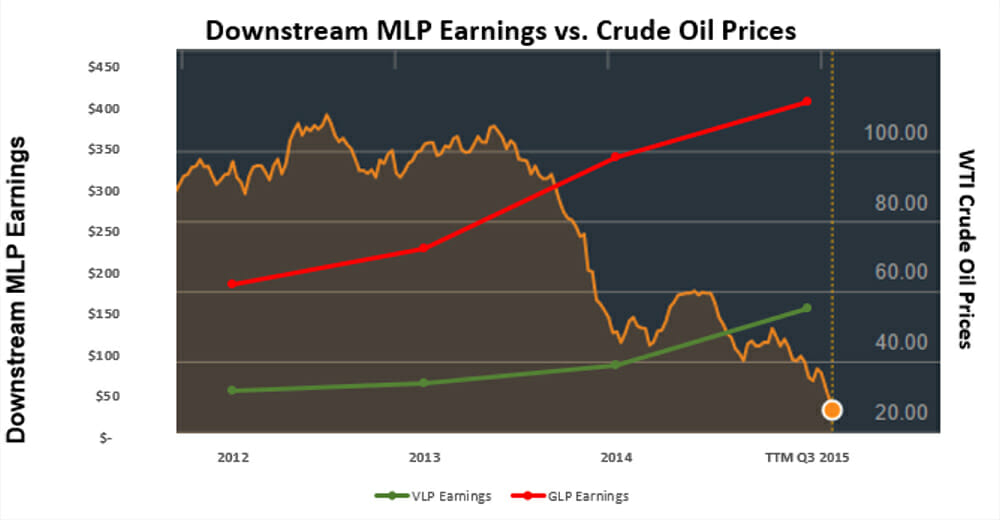

During the crash in oil prices from 2014 till now, most energy MLP units have taken a beating, painted with the “crude decline” brush, regardless of whether the assets are classified as downstream, midstream, or upstream. Oil is a feedstock (or input product) for downstream companies, and fuel (both wholesale and retail) prices tend to change slower with respect to feedstock prices. More importantly, downstream MLPs work on a fairly predictable and ratable margin structure, which is not correlated to crude prices. As a result, downstream MLPs have been experiencing healthy margins with the sharp sell-off in crude. In spite of downstream MLPs actually growing their net income over the past year, their units are still under heavy pressure. In summary, the fundamental performance factors for downstream MLPs have not changed, or perhaps even strengthened on a short term basis, in spite of their units not trading well in the market place.

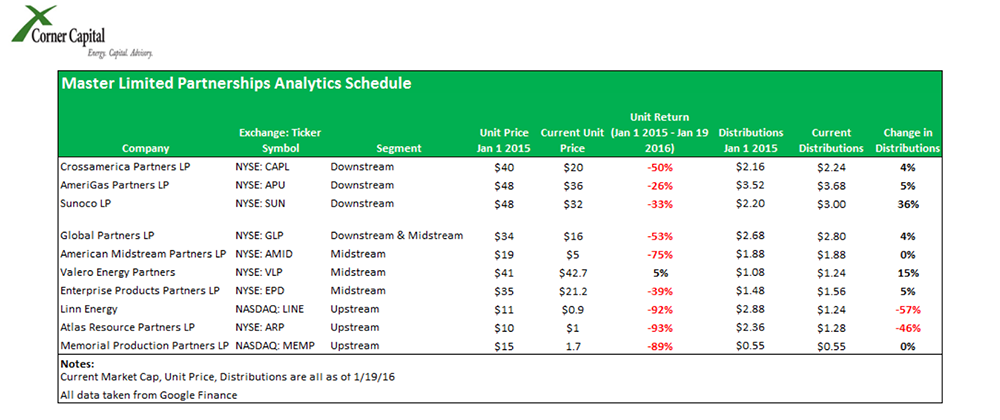

Regardless of the strong quality earnings for downstream MLPs, investment managers generally seem to be exiting all energy-related investments. Accounting for the macro pull back in equity prices from volatile markets abroad (i.e. Chinese circuit-breakers & uncertain monetary policy), 2015 and 2016 so far has not been a good period for MLP unit-holders, regardless of their focus with respect to the energy supply chain. The table below shows a breakdown of MLP unit performance by Company and Segment (downstream, midstream, or upstream).

Since early 2015, upstream MLPs have been demolished with average unit price declines of 91%, and have cut distributions to meet their debt-servicing mandates. Most downstream and midstream MLPs have also experienced significant declines in their unit prices, falling 25%-50%. However, the downstream and midstream MLPs are actually increasing their distributions since they have more cash to distribute from increased margins during this time period of falling crude (feedstock), and their need to increase unit prices. Average distribution yields on downstream MLP’s have increased by nearly a factor of 2 from 8% in early 2015 to 15% currently.

WHAT DOES THIS MEAN FOR DOWNSTREAM MLPS’ ACQUISITION ACTIVITY IN 2016?

There are two ways that a downstream MLP can grow: organically or via acquisitions. Organic growth comes from expanding EBITDA via increased margins, reduced expenses, and reserving capital for New To Industry ground-up stores and dealer supply locations. Acquisition growth results from purchasing new assets to grow the bottom line, while generally adding only variable costs to its infrastructure. The most rapid growth method is acquisition, and usually the most rewarded in terms of future outlook and unit prices.

As industry fuel margins eventually stabilize and downstream MLPs continue to offer higher than normal distributions, it will be difficult for MLPs to experience organic growth. It’s our view that acquisition growth will continue to be the primary driver for downstream MLPs’ growth in 2016. However, we do expect that acquisition values will plateau and perhaps decline on an EBITDA multiple basis in the coming year. Yet this process will be beneficial to downstream MLPs, their balance sheets, and their earnings. While Enterprise Value / EBITDA multiples have been strong in the downstream sector, competition for high quality assets will likely persist in 2016. We also believe that there will eventually be a shortage of high-quality, long-term retail assets available for acquirers of retail assets, as those retail buyers (MLPs and national franchise chains) will have picked the “low-hanging fruit”.

In order to finance acquisitions at competitive valuations, downstream MLPs can either tap into existing debt facilities, obtain additional credit, or issue units in the capital markets. Since MLP units are trading at low levels historically, it would be costly for downstream MLPs to raise funds by issuing equity. Therefore, we anticipate the expected robust M&A activity by downstream MLPs in 2016 will be financed by existing or newly secured debt facilities.

In summary, while unit prices for downstream MLPs have fallen over the past year, fundamental performances contradict this decline. The myriad of factors from sharply falling crude and macro-level volatility has put a damper on the energy sector, regardless of the segment. However, given the likelihood that downstream MLPs will continue to seek high quality assets in order to grow their bottom line, we expect M&A activity by downstream MLPs to continue in 2016. Since unit prices are currently low relative to historic values, it’s likely that the upcoming acquisitions will be financed by debt.

For any feedback or questions, please contact Kevin Henrick at the contact information below:

Kevin Henrick

812 Anacapa Street, Suite A

Santa Barbara, CA 93101

(805) 965-5510 w

(646) 673-4623 c

www.cornercapitalpartners.com